-

The IRS often challenges “inter vivos” transfers of property that reduce estate tax liabilities and a common issue is whether there was a bona fide business purpose or if it was simply a pretext to avoid taxes.

-

A poorly conceived transfer, however, can lead to advers financial consequences through accuracy-related penalties, which were assessed here against the estate for underpayment of tax.

-

The timing of the transfers is a key consideration and will be examined to determine if there was was a bona fide reason for the transfer.

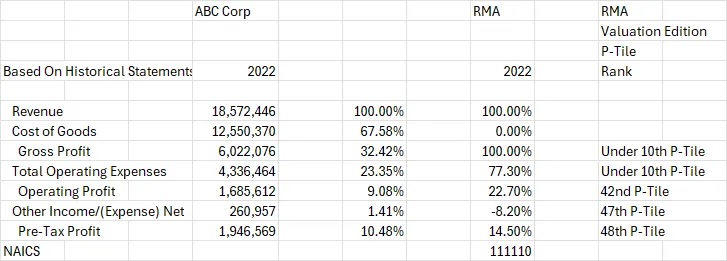

Transfers of business interests routinely seek to benefit from the discounts that accompany lack or control and marketability. Reducing the assets in an estate obviously reduces estate tax liability and the application of discounts in the transfer made during one’s life can result in significant tax savings.

The IRS, howevechallenges these “inter vivos” transactions, and a common issue r, often is whether there was a bona fide business purpose or if it was simply a pretext to avoid taxes.

On this issue, timing may be everything. And the price if missteps is significant.

The Tax Court’s decision in Estate of Fields v. Commissioner of Internal Revenue, illustrates how timing, retained interests, and procedural missteps in estate planning can lead to significant tax liabilities.

The opinion is discussed in detail in my post on the

The case also underscores the potential financial consequences through accuracy-related penalties, which were assessed here against the estate for underpayment of tax. We take a look here at the facts, procedural history, legal principles, the 20 percent penalty assessment, and the key takeaways for estate planning professionals.

As the Tax Court judge noted, if the strategy is too good to be true, it probably is.

Key Facts: Ms. Fields’ Life, Assets, and Planning

Anne Milner Fields, a Texas resident, built considerable wealth managing an oil business she inherited from her late husband. By 2016, Ms. Fields was 91 years old, battling Alzheimer’s, and reliant on her great-nephew Bryan Milner to manage her financial affairs. Mr. Milner held a power of attorney and implemented an estate planning strategy just a month before Ms. Fields passed away.

business after 2012 would proceed.

business after 2012 would proceed.

In

In